C3.ai - Investment Thesis and Future Outlook

A business-side introduction to C3.ai covering its pain points, products, go-to-market strategy, financial profile, competitive advantages, and future outlook.

- Hank

- 12 min read

English Version (中文版本在下方)

This article is an introduction to and analysis of C3.ai from the business and operating side. If you want to understand its technical features, please refer to this article.

Preface

In 2020, even though the whole world was still under the shadow of the pandemic, the US stock market kept reaching new highs. Many IPO stocks soared after listing, and in the second half of 2020 alone, as many as 16 enterprise software companies successfully went public in the United States. With multiple AI, big data, and cloud-related companies going public one after another, many analysts and media outlets described 2020 as the start of a new paradigm shift in US equities, calling it the “first year of cloud computing.”

The best-known example may have been Snowflake, the cloud data platform that even Warren Buffett invested in heavily. But the company I want to discuss here is less well known and yet closely tied to future technology trends such as AI, big data, and cloud computing. That company is C3.ai, which went public at $42 on December 9, 2020, immediately rose by more than 100 percent, and then climbed to around $150, a gain of more than 250 percent.

This article will give a simple introduction to C3.ai’s pain points, products and services, go-to-market strategy, financial analysis, competitive advantages, and future outlook, in the hope of helping readers better understand the company’s past, present, and future.

Company Overview

C3.ai was founded in 2009 by Tom Siebel. It is an enterprise AI software company that provides software-as-a-service applications. These applications can rapidly deploy large-scale and complex enterprise AI use cases, enabling companies in the middle of digital transformation to build and use their own AI applications more quickly and more easily.

The predecessor of C3.ai was C3 IoT. Its original purpose was to drive digital transformation in the traditional energy industry. The approach was to use tens of thousands of sensing devices to detect and collect data from energy extraction equipment, then perform analysis on that data for energy management.

But after the wave of AI enthusiasm arrived, C3.ai successfully repositioned itself as a provider of AI transformation services for enterprises. Drawing on its expertise in the energy industry, it built highly customized industry solutions so that enterprises could create and deploy AI environments and applications in the shortest possible time.

C3.ai initially focused on manufacturing and Industry 4.0, where it became especially familiar with commercial applications and analysis related to factories and IoT. As the company expanded, it also began bringing more industries into its commercial scope, hoping to help companies across sectors carry out AI-related transformation.

Pain Point

The birth of a service often begins with the intention to solve a problem, and C3.ai exists to solve the pain enterprises face when trying to adopt and use AI technologies.

Although most people understand the breakthrough potential of AI and machine learning, both still face major difficulties in practical business applications. Because of entrenched habits and legacy systems, traditional enterprises often run into serious technical challenges during digital transformation.

Traditionally, if an enterprise wanted to develop its own AI application environment, the standard approach required building many different connections among applications, data sources, AI models, and machine learning libraries. That approach is complex, expensive, and very time-consuming. It also requires writing a large amount of code, which often leads to systems that are difficult to maintain. In the end, such an environment is neither economically efficient nor capable of meeting quality expectations.

By contrast, C3 AI Suite greatly accelerates and simplifies the design, development, and operation of enterprise AI and machine learning applications. It uses a unique cloud-native and model-driven architecture to provide a mature, cross-industry AI and ML software solution.

The suite allows users to quickly design, develop, deploy, and operate enterprise AI and IoT applications at scale, while integrating the necessary technologies and functions into one aggregated model-driven software architecture.

Products and Services

On the product side, C3.ai mainly provides two things: C3 AI Suite and C3 AI applications.

At the core, these two offerings are really part of one integrated service. C3.ai first provides the environment that allows enterprises to develop AI applications. It then sells AI analytics applications that run on top of that environment. Together, these two layers help enterprises quickly transition into an AI-driven digital environment and immediately begin running AI programs that generate useful analysis and feedback.

Go-to-Market Strategy

To talk about C3.ai’s go-to-market strategy, you have to mention its founder, Tom Siebel. Tom founded the famous Siebel Systems in 1993, and that company later merged successfully with Oracle in 2006. Siebel Systems was dedicated to building CRM systems and strongly promoted the digital transformation of sales and marketing departments. Salesforce, one of today’s major technology leaders, was only founded in 1999, which means it entered the CRM field even later than Siebel Systems. That alone shows how forward-looking Tom Siebel’s technology instincts were.

As a successful technology founder, Tom Siebel’s background also played a major role in shaping and executing C3.ai’s market-entry strategy. Because asking enterprises to shift from traditional operations to AI-based operations is not easy, C3.ai decided to start with flagship companies in target industries.

C3.ai helped “lighthouse customers” in various sectors undergo AI transformation, used those wins to establish a leading position in each domain, and then promoted those successful use cases as customer stories. This resembles IBM’s historical sales approach in many countries: first sell supercomputers to governments and public institutions, then to large enterprises, and only later move down to ordinary small and medium-sized companies, creating a top-down diffusion effect.

Of course, this strategy has an obvious early difficulty: how does an unknown startup win large enterprise orders at the beginning? This depends to a large extent on Tom Siebel’s experience and network.

Because Tom Siebel is a well-known Silicon Valley entrepreneur, his network has helped C3.ai reach senior decision-makers at major corporations. On top of that, Siebel Systems’ past success in helping many large enterprises digitally transform their sales departments gave C3.ai powerful credibility. That allowed the company to expand its early business and grow to its current scale. But whether it can keep reproducing this strategy in the future remains an important uncertainty for its growth engine.

Financial Analysis

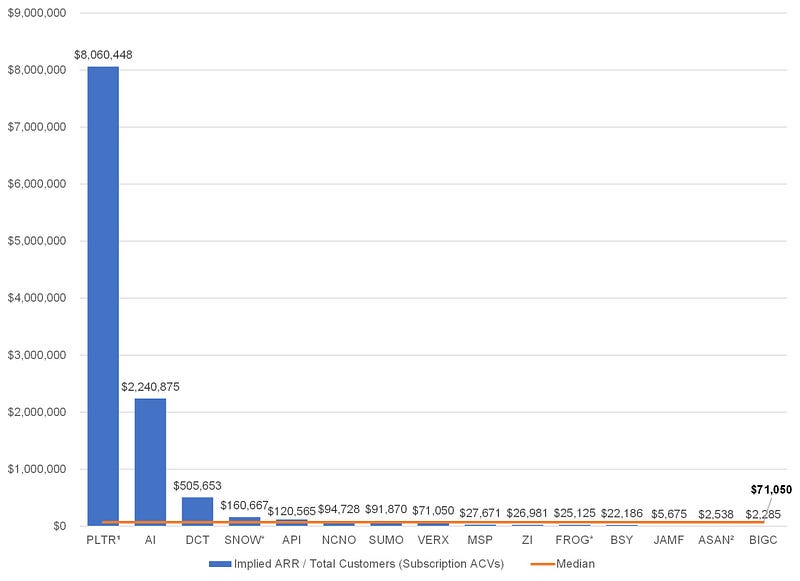

That sales strategy is also reflected in the financial profile. Because C3.ai’s customers are mostly large enterprises, its overall average contract value reached $2,240,875 in implied ARR per customer. Among the roughly ninety-plus SaaS companies in the US public market, only Palantir, which also prioritizes large customers, exceeds C3.ai on that metric, at $8,060,448. This shows how strong C3.ai’s average deal size has been.

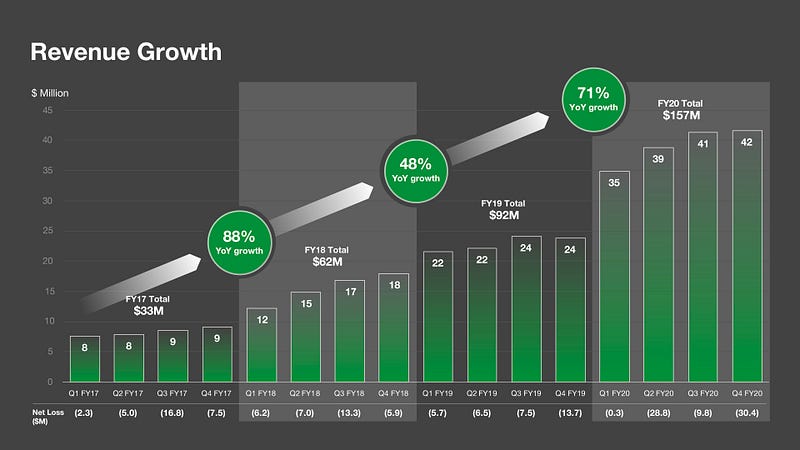

Looking at contracts signed from 2016 to 2020, C3.ai’s average total contract values were $1.2 million, $11.7 million, $10.8 million, $16.2 million, and $12.1 million respectively. The drop from 2019 to 2020 was significant, which shows that the company cannot count on landing similarly large contracts every year.

In terms of business growth, even though annual growth in 2019 and 2020 reached about 71 percent, a closer look shows that as of the quarter ending July 2020, C3.ai’s quarter-over-quarter growth was only 6.3 percent, which is weak relative to the average 39.7 percent quarterly growth seen across the 16 B2B companies that went public in 2020.

One reason for that is high customer concentration. The top three customers, including Baker Hughes, accounted for 44 percent of revenue. This reliance on a narrow revenue base is a major operating issue C3.ai needs to improve in the short term. Although the company says it will use its success with large enterprises as an entry point and then expand into the mid-market through direct sales, inside sales, and heavy advertising, it still remains to be seen whether that will work.

In addition, both R&D expense and sales and marketing expense show excessive volatility for a public company. Sales and marketing expense in particular fluctuated between 35 percent and 83 percent in the most recent three quarters. This instability is likely to continue until C3.ai finds an effective path into the mid-market.

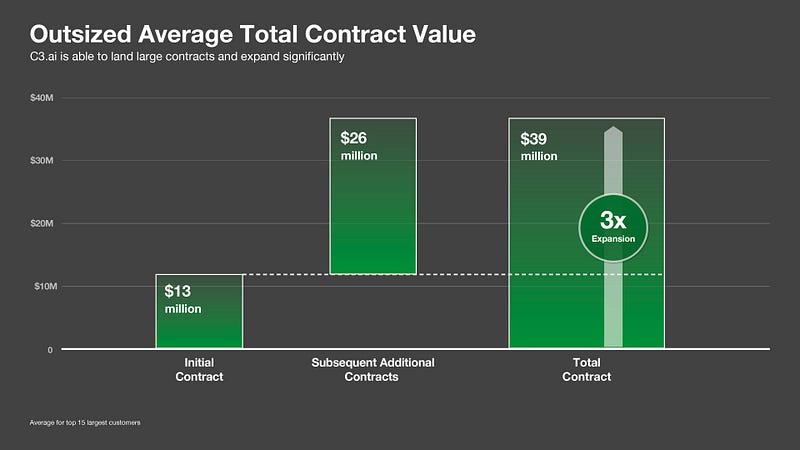

As for customer retention, while C3.ai did not disclose a specific figure, the prospectus states that its fifteen largest customers had an average initial contract value of $12.8 million. By 2020, those same customers had on average spent an additional $26.1 million each on products and services as their use of and dependence on C3.ai deepened. That suggests AI’s impact on enterprise operations is both significant and difficult to reverse. Once customers experience concrete results, spending tends to remain stable and even expand.

Despite the concerns above, the size of the market C3.ai sits in can solve many worries at once. The enterprise AI market C3.ai operates in was expected to reach $174 billion in 2020 and grow to $271 billion by 2024, implying a 12 percent compound annual growth rate. When you stand in front of a powerful tailwind, even pigs can fly, and C3.ai is not just any pig but a company with strong potential, so it is not hard to understand why the market has high expectations for it.

Competitive Advantage

C3.ai’s prospectus says that one of its biggest competitors is the enterprise customer trying to build an AI environment internally, because many of those efforts eventually fail from being too time-consuming and expensive. In the integrated AI environment and applications category, the company even says it has not yet found any direct competitor. Looking at G2, the enterprise software review site, it does appear that there are still no fully identical competitors providing the same integrated offering. Most players in the market are still focused on project-based enterprise AI solutions. C3.ai’s model-driven foundation gives it maximum compatibility with AI development, allowing it to provide a scalable, unified AI environment and application solution that other players in this space have not really matched.

Over the past decade, the company’s heavy investment in products and technology has given it a clear first-mover advantage in enterprise AI. In the manufacturing and industrial domains where C3.ai is strongest, it has also become the world’s largest large-scale big data, predictive analytics, and IoT application provider, with more than 100 million connected sensors and devices. In addition, C3.ai has repeatedly appeared on CNBC’s Disruptor 50 list and has received recognition from CB Insights AI 100 and Forbes Cloud 100, all of which reflect the depth of its position in this field.

Future Outlook

Because of Tom Siebel’s background, I cannot help repeatedly comparing C3.ai with Salesforce. In terms of vision, both aim to help enterprises with digital transformation. In go-to-market strategy, both start with large enterprise customers and then gradually move downward into broader markets. In addition, both companies offer new kinds of services: C3.ai provides integrated AI solutions, while Salesforce provides SaaS-based CRM systems. Overall, both were highly distinctive and novel offerings for their time.

In terms of broader market conditions, C3.ai was operating in 2020, a year many people called the beginning of the cloud-computing era. Riding the wave of 5G, IoT, and big data, AI applications in business analysis also looked increasingly attractive. Salesforce, by contrast, emerged at the beginning of the internet era, when the digitization of enterprise operations was accelerating rapidly, and the transformation of sales departments became one of the major pain points it could solve. Maybe the comparison is only a coincidence, but the parallels still provide useful clues about C3.ai’s possible future.

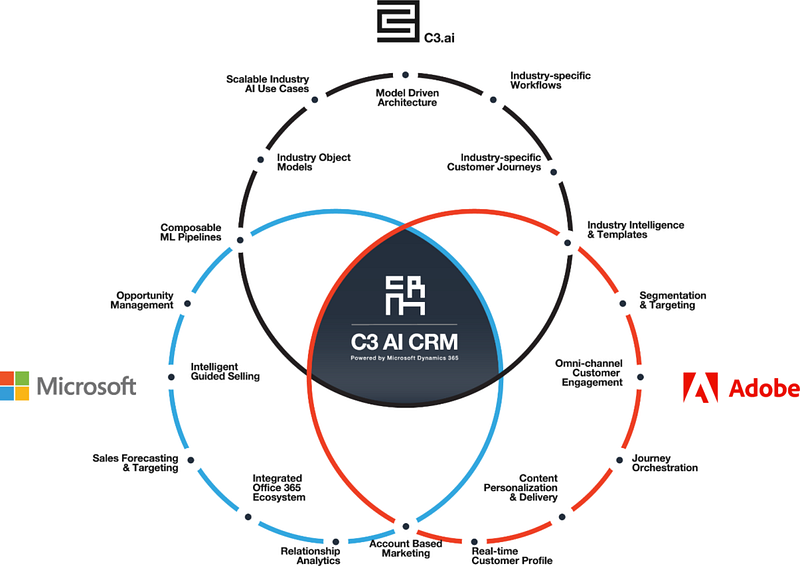

More recently, C3.ai also launched C3 AI CRM in partnership with Microsoft’s ERP and CRM platform Dynamics 365 and Adobe’s marketing and web analytics platform Adobe Experience Cloud, with the goal of helping enterprise sales teams carry out a second wave of digital transformation. It looks like the pioneers of two different generations may soon be fighting on the same battlefield.

Coming back to reality, I still believe C3.ai can become a large and successful company in the future, as long as it can prove that its strategy for moving into the mid-market is workable. If over the coming quarters and years the company succeeds in penetrating small and medium-sized businesses through its sales channels, then the high customer concentration and slowing revenue growth problems could be substantially reduced. But it will also be important to watch whether mid-market revenue has strong retention characteristics and whether the decline in average contract value remains within a reasonable range.

Taken together, C3.ai’s sales and marketing performance this year will be the key factor determining whether it can move to the next level, and reducing operating volatility will be another major challenge.

This article only shares my own views and opinions. It is not an investment recommendation. Its purpose is simply to provide a more detailed introduction to C3.ai based on available information and numbers. If there are weaknesses in the argument or errors in the evidence, discussion is welcome. Thank you for reading.

淺談 C3.ai 投資亮點與發展前景

中文版本

此篇為 C3.ai 公司營運相關的介紹與分析,若想瞭解其技術方面的特點請參閱這篇文章!

前言

2020 年,雖然全世界依舊深陷疫情的陰霾之中,然而美國股市卻一再創下新高,其中多檔的 IPO 股票更是在上市後一飛沖天,光是 2020 下半年美國便有高達 16 家提供企業軟體服務的公司成功上市。而多家 AI、大數據、雲計算相關的企業接連公開發行,使得眾分析師與媒體稱 2020 年為美股近代典範轉移的開端,是為「雲計算元年」。

其中最為人所知的,應是股神巴菲特也重金買入的雲端數據平台 Snowflake,而今次要介紹的主角則是知名度相對沒那麼高,但卻與 AI、大數據、雲計算……等未來科技趨勢有十分密切的關聯,這家公司便是在 2020 年 12 月 9 日以 42 美元上市但隨即上漲超過 100 %,如今其價格已飆升至 150 元上下,漲幅超過 250 % 的 C3.ai。

本文會就 C3.ai 的痛點、產品服務、營銷策略、財務分析、競爭優勢、和前景發展進行簡單的介紹,希望能帶大家更了解此公司的過去、現在、與未來。

公司簡介

C3.ai , 2009 年由 Tom Siebel 創立,是一家企業 AI 軟體公司,提供軟體即服務(SaaS)應用程式。這些應用程式可以快速部署大規模和複雜的企業 AI 應用程式,並使企業在數位轉型中,快速且簡單地開發並應用屬於自身的 AI 應用。

C3.ai 前身是 C3 IOT,最先創立的初衷是將傳統的能源產業進行數位轉型。其作法是使用數以萬計的感知裝置偵測並蒐集能源開採設備的資料,藉由資料分析進行能源管理。

但在 AI 風潮的來襲後,C3.ai 則順應熱潮成功轉型成提供企業進行 AI 轉型的服務供應商,其利用在能源產業的專業知識打造高度客製化的產業解決方案,讓企業能夠在最短的時間建構並部屬 AI 環境與應用程式。

C3.ai 最初以製造業與工業 4.0 為主要發展的產業別,對於工廠、物聯網 IoT 相關領域的商業應用與分析十分熟悉,隨著企業擴張後也開始將各行業別納入商業版圖,希望協助各行各業的企業體進行 AI 相關的轉型。

痛點

一個服務的誕生往往始於解決一個問題的初衷,而 C3.ai 的存在便是為了解決企業在導入與使用 AI 科技的痛點。

儘管大多數的人都明白 AI / ML 將帶來的突破,但兩者在商業應用上卻始終面臨巨大的難處。由於過往習慣的僵固,傳統企業在數位轉型上經常面對許多技術上的困難。

傳統上,企業若要自行開發 AI 應用環境,典型方法便需要在應用程式、數據源、AI 模型、和機器學習庫之間建立大量且多種的連接,這種方法複雜、昂貴並且非常耗時。此外,也需要編寫大量程式碼,而此舉往往會導致難以維護的應用程式與環境,最終既不符合經濟效益也無法滿足品質上的需求。

相比之下,C3 AI Suite 極大地加速並簡化了企業 AI / ML 應用程式的設計、開發、及操作。C3 AI Suite 利用獨特的雲原生(cloud-origin)和模型驅動的架構為企業提供一套成熟且跨行業的 AI / ML 軟體解決方案。

該套件使用戶能夠快速大規模地設計、開發、部署、操作企業 AI 和 IoT 應用程式,並將必要技術和功能整合到一個聚合的模型驅動軟體架構。

產品服務

產品面,C3.ai 主要提供兩種服務,分別是 C3 AI Suite 和 C3 AI 的應用:

此兩樣應用在根本上是一體的服務。C3.ai 首先提供企業能夠開發 AI 應用的環境建構,隨後便會再向其推銷在此環境上運行的 AI 分析應用程式。兩者相輔助下便能使企業快速轉型至 AI 數位環境並直接運行 AI 程式,進而立即得到其帶來的分析數據與反饋。

營銷策略

要談到 C3.ai 的市場營銷策略便不得不提及其創辦人 Tom Siebel 。Tom 曾在 1993 年創立著名的 Siebel Systems,此公司在 2006 年與甲骨文順利合併。Siebel Systems 致力於開發 CRM 系統,並為銷售與行銷部門的數位轉型不遺餘力。而現今為科技龍頭之一的 Salesforce 則是在 1999年才創立,甚至比 Siebel Systems 還晚踏入 CRM 領域,由此也可看出 Tom Siebel 對於科技趨勢的眼光有多前瞻。

作為一成功的科技創業家, Tom Siebel 的背景也很大程度幫助了 C3.ai 在市場進入策略上的制定與執行。在營銷策略上,由於需要使企業從傳統營運模式轉型使用 AI 並不是一件易事,因此 C3.ai 決定先從目標行業的指標性企業下手。

C3.ai 藉由協助各領域的「燈塔用戶」進行 AI 轉型,藉此豎立其在各領域的領先地位,並將這些成功的使用案例作為顧客故事加以宣傳。此案例與過去 IBM 在各個國家的銷售手法一致,先將超級電腦出售給政府公部門,再來是大企業,最後才是一般中小企業,以此進行由上至下的擴散式行銷。

然而此策略存在最初的困難點,一家默默無名的新創企業將如何在初期便取得大型客戶的訂單?此點便很大程度依賴創始人 Tom Siebel 的經歷與人脈了。

由於 Tom Siebel 為一知名矽谷創業家,因此在人脈網絡上能很大程度為 C3.ai 牽線到大型企業的高層,而 Siebel Systems 過去成功幫助多家大企業在銷售部門的數位轉型經驗也形成 C3.ai 強而有力的背書,使的 C3.ai 能順利拓展初期業務,並成長至現今規模。但未來能否持續複製此策略將會是其業務增長動能的一大隱憂。

財務分析

而此銷售策略也反映在財務面上,由於 C3.ai 的客戶大多為大型企業體,其整體的平均訂單金額達到$2,240,875 美元(Implied ARR / Total Customers),綜觀美國股市上 90 幾家的 SaaS公司,幾乎只有同樣以大型客戶為優先的 Palantir,以$8,060,448 美元超過 C3.ai,由此可見 C3.ai 在平均訂單金額上的優異表現。

而 C3.ai 在 2016 至 2020 年簽訂的合約中,分別的平均總合約價值為 120 萬美元,1170 萬美元,1080 萬美元,1620 萬美元和1210萬美元。在 19 年到 20 年出現了顯著的下滑,也顯示其無法保證每年皆有相同的大筆金額訂單。

在業務增長方面,儘管 19、20 年的年增長率有 71 %的水平,但仔細觀察便會發現 C3.ai 在結至 2020 年 7 月底的季增長率只有不及格的 6.3 %,相較於 2020 年上市的 16 家 B2B 公司平均的 39.7 % 季增長率,表現可謂差強人意。

而上述的發現可歸因於客戶集中度過高的問題,包含 Baker Hughes 等前三大客戶便佔了營收的 44%,營收來源的單一將是短期內 C3.ai 需改善的營運重點,儘管 C3.ai 聲明將以大企業的成功案例作為切入點,並利用直接銷售、電話銷售、與大量的廣告策略開拓中端市場,但能否如願達成還需時間觀望。

另外,在研發費用、銷售和行銷費用中,兩者的變化幅度在上市公司都存在波動太大的問題,尤其銷售和行銷費用在最近三個季度在 35–83% 間變動,預計這樣的不穩定性將會持續到 C3.ai 找到切入中端市場的有效途徑。

在顧客留存比率上,雖然 C3.ai 並未實際提供數字,但在招股書上提到其最大的 15 位顧客平均初始合約金額為 1280 萬美元,而隨著客戶對於 C3.ai 產品的使用與依賴,到 2020 年為止,這 15 位客戶中平均每位會再消費額外的 2610 萬美元進行產品訂購與服務。這可視為AI 對於企業的影響是巨大且無法回復的,一旦體驗過其所帶來的實際成果,客戶將穩定且上升的持續消費。

儘管存在上述隱憂,但 C3.ai 身處的龐大市場仍會是一切的百憂解。C3.ai 所在的企業 AI 市場預計在 2020 年將達 1,740 億美元,到 2024 年將增長至 2,710 億美元,複合年增長率(CAGR)為 12%。站在風口上,連豬都會飛,更何況 C3.ai 還是一潛力極佳的公司,市場對其懷抱濃厚希望也就不難想像了。

競爭優勢

在 C3.ai 的招股書上寫著,他們最大的競爭是企業打算自己動手建造 AI 環境,但企業們最終也都會因為耗時耗力而失敗。另外在 AI 環境與應用的系統服務上,他們甚至還未發現任何對手。從 G2 網站(企業軟體評價網)中可發現 C3.ai 確實還未出現完全提供相同服務的競爭對手,目前業界大多都還停留在提供企業 AI 專案式的解決方案,且其模型驅動的本質能夠與 AI 開發達到最大程度的相容,從而提供可規模化的一體式 AI 環境建構和應用解決方案,這也是其他此領域的玩家所無法達到的。

在過去十年的發展中,C3.ai 在產品和技術方面的大量投資使其在企業 AI 方面享有明顯的先進者優勢。在 C3.ai 熟悉的製造業與工業相關領域,C3.ai 也以超過 1 億個感應器與裝置,成為全球最大的大規模大數據、商業預測分析、和物聯網應用提供商。另外,C3.ai屢次入選 CNBC Disruptor 50 的榜單,多次獲得 CB Insights AI 100 和 Forbes The Cloud 100 的評比,這些也都是他在此領域擁有深厚底蘊的展現。

前景發展

由於 Tom Siebel 的背景,我不可避免地一再將 C3.ai 與 Salesforce 互相比較。願景上,兩者都一樣以協助企業的數位轉型為己任;在營銷策略上都先以大型企業客戶做為切入點,再慢慢向下滲透至所有市場;除此之外兩家企業都提供新型態的服務,C3.ai提供一體化 AI 解決方案,Salesforce 則提供 SaaS 形式的 CRM 系統,總的來說,兩者在當下都是十分獨特且新穎的產品服務。

在大環境方面,C3.ai 身處被譽為雲計算元年的 2020 年,由於搭上 5G 將帶來的物聯網、大數據時代的浪潮,使得在 AI 在商業分析的應用也隨之看好;而 Salesforce 當時處在互聯網時代的開端,企業各營運流程的數位化正在高速發展階段,而銷售部門的轉型問題便成為 Salesforce 解決的企業痛點。也許僅是巧合,但兩者之間的對比參照,依舊能推斷出不少 C3.ai 未來發展的端倪。

近期 C3.ai 也結合微軟 ERP/CRM 平台 Microsoft Dynamics 365,和 Adobe 的網路行銷及網頁分析平台 Adobe Experience Cloud 共同推出 C3 AI CRM 服務,旨在協助企業銷售進行第二次的數位轉型,看來兩新舊時代的開拓者近期勢必將有一場同一戰場的龍爭虎鬥。

回到現實面,我依舊認為 C3.ai 在未來發展上會是大型且成功的公司,只要此公司能證明其在營銷策略上向中端市場切入的可行性。若接下來幾季甚至年,C3.ai 在銷售管道上,滲透中小企業的策略能成功,則客戶集中度高與營收增長漸緩的問題將一筆勾消,C3.ai 離成功也就不遠了,惟將謹慎注意中端市場帶來的營收品質是否存在高留存率的特質,也需重點檢視中端市場的平均訂單金額下滑的百分比是否在合理區間。

綜合以上,C3.ai 今年的銷售與行銷能力將是決定其能否再上一層樓的關鍵,同時降低營運上的波動度也是重要課題。

此篇文章僅分享筆者本身的看法和觀點,並不作為投資標的的推薦,旨在根據資料和數字帶給大家關於 C3.ai 更詳細的介紹,如有論述不足或舉證錯誤的地方也歡迎提出討論,感謝大家耐心的閱讀。

- Tags:

- Technology

- Ai

- Startups