Taiwan Energy Policy: Renewable Constraints and Rethinking Nuclear Power (2025 Edition)

In 2021, I wrote an essay on Taiwan's energy transition using international power mixes as a reference point. Four years later, the global energy landscape, technology costs, and policy attitudes have all shifted, and Taiwan now faces a new crossroads.

- Hank

- 6 min read

English Version (中文版本在下方)

Introduction

In 2021, I wrote an earlier piece, Energy Policy: The Constraints of Renewable Energy and the Nuclear Tradeoff, using international energy structures as a reference for Taiwan’s transition path. Four years later, the global energy landscape, technology costs, and policy attitudes have all changed dramatically. Taiwan now faces a new crossroads: renewable deployment is slower than expected, dependence on natural gas has deepened, and the referendum on extending Nuclear Plant No. 3 has become a political focal point.

In this article, I use the 2021 analysis as a starting point, extend the framework with ChatGPT, and integrate updated international data, Taiwan’s current conditions, and the latest policy disputes. The result is this 2025 edition: part review, part attempt to outline a more concrete and workable energy strategy for the future.

National Energy Mixes in 2024

As usual, it makes sense to start with a cross-country comparison. I recommend this site if you want to explore national electricity mixes directly. It is one of the clearest summaries available.

United States:

“The shale gas advantage remains intact. Natural gas still accounts for roughly 40 percent, wind and solar continue to grow, and nuclear stays stable at around 20 percent.”

Natural gas about 39%, nuclear 19%, renewables 23%, coal 18%.

European Union:

“Zero-carbon power remains the main direction. Wind and solar are rising quickly, and multiple countries are reassessing the role of nuclear power.”

Renewables 42%, nuclear 24%; among fossil fuels, coal and natural gas account for roughly 15% and 19%.

Germany:

“Germany has fully exited nuclear power. Wind and solar together exceed half of generation, while coal has seen a short-term rebound due to energy security concerns.”

Renewables 52%, coal 27%, natural gas 17%.

France:

“Still the country with the highest nuclear share in the world.”

Nuclear remains dominant at 68%. Renewables are about 24%, coal 2%, and natural gas 6%.

Japan:

“Japan has restarted multiple nuclear reactors and now treats nuclear as dual insurance for decarbonization and energy security.”

Renewables 25%, nuclear 10%, natural gas 28%, coal 27%.

South Korea:

“Korea is extending the service life of nuclear units while also promoting offshore wind.”

Nuclear 27%, renewables 8%, coal 35%, natural gas 28%.

Taiwan’s Energy Situation in 2024

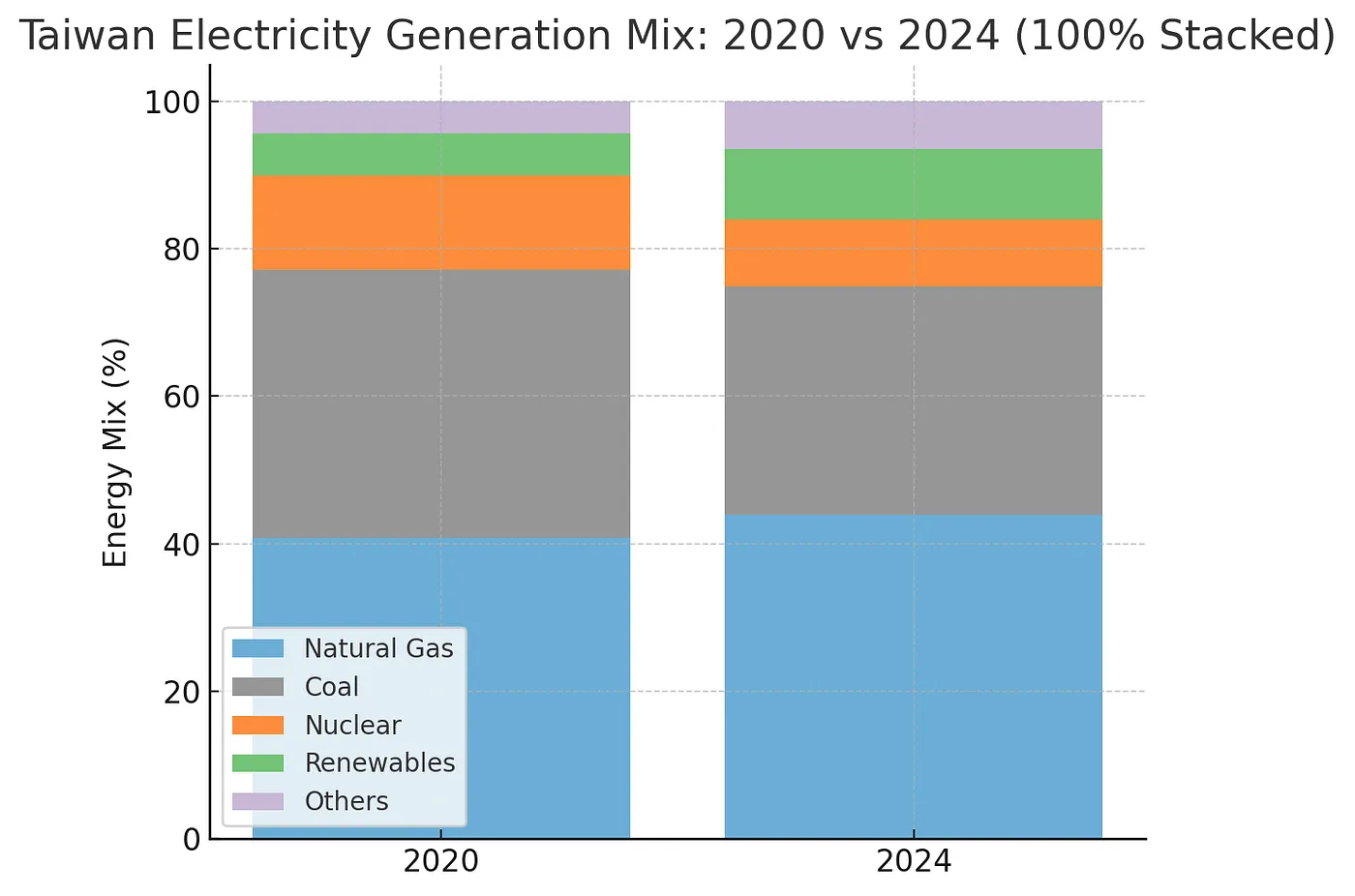

- Natural gas: about 44% (up from 40.8% in 2020)

- Coal: about 31% (lower than before, but still above 30%)

- Nuclear: about 9% (after Nuclear No. 2 retired and Nuclear No. 3 was decommissioned)

- Renewables: about 9-10% (offshore wind 2-3%, solar 5-6%)

- 2024: natural gas 44%, coal 31%, nuclear 9%, renewables 9.5%, other about 6.5%.

- 2020: natural gas 40.8%, coal 36.4%, nuclear 12.7%, renewables 5.8%, other about 4.3%.

Observations

- Renewable energy has roughly doubled its share compared with three years ago, but it still falls far short of the official 20% target for 2025.

- Taiwan remains highly dependent on imported natural gas and is heavily exposed to global LNG price volatility.

- Debate over extending Nuclear No. 3 has intensified, but clear implementation detail is still lacking.

Energy-by-Energy Analysis and My 2025 Position

Thermal Power

- Natural gas will remain the core baseload source in the near term, likely 40-45% during 2025-2030, while coal should be pushed below 25%.

- Taiwan should use longer-term LNG contracts to reduce exposure to import-price volatility.

Renewable Energy

- Short-term target: raise the renewable share from 9.5% to 20% between 2025 and 2030.

- Grid expansion and energy storage need to accelerate in parallel so that renewable generation is not wasted because the grid cannot absorb it.

- Electricity pricing should be rationalized, directing subsidies toward infrastructure instead of focusing only on expensive power-price support.

Nuclear Power

- I do not support extending Nuclear No. 3 or restarting Nuclear No. 4. The key issue is not political slogan-making, but time and cost. Based on the historical documentation process for Nuclear No. 1, the safety review alone took seven years. If that precedent is meaningful, extending Nuclear No. 3 would not close Taiwan’s near-term supply gap in time. Restarting Nuclear No. 4 faces the same problems: long timelines, high technical barriers, low social acceptance, and unresolved safety concerns.

- Strategic direction: Taiwan should stop allocating major resources to large traditional nuclear plants. Instead, research and policy attention should shift toward next-generation options such as small modular reactors, which may provide stable low-carbon backup after 2035.

Recap of My 2021 Observation

On Nuclear No. 4

Setting aside the still-controversial engineering and safety questions, my focus was on the broader direction of energy planning and whether restarting Nuclear No. 4 was actually necessary.

At the time, renewables contributed around 5-6%, while restarting Nuclear No. 4 was expected to contribute another 5%. Nuclear No. 4 could act as baseload power, but Taiwan already had natural gas and coal for stability, so the system was not lacking baseload generation. That meant the real question was the restart timeline versus the growth rate of renewables.

The awkward position of Nuclear No. 4 was that if it could not be restarted quickly enough to bridge the retirement of Nuclear No. 2 and No. 3, Taiwan would hit zero nuclear in 2025 and then suddenly add 5% back around 2030. That kind of jump would make energy planning more difficult. Aside from Japan, which changed its domestic nuclear stance after Fukushima, I did not see many countries making sharp U-turns in their nuclear policy.

Looking at how renewables developed globally, it was clear that with strong government support, doubling within ten years was not unusual. Many countries moved from around 10% to 20% during the decade from 2010 to 2020. Taiwan’s natural conditions are not weak, especially in wind and solar, and its renewable base was still relatively low. Reaching 10% within ten years did not look impossible. If Nuclear No. 4 required seven years to restart and would only add 5%, then renewables doubling in that same period could fill the gap. If growth proved too slow, extending Nuclear No. 3 could buy time. In other words, the only reasonable case for extending Nuclear No. 3 would be if renewable deployment seriously underperformed.

Conclusion

Taiwan’s energy transition cannot be solved by a single source. The 2025 referendum on extending Nuclear No. 3 may draw political attention, but the real problem is how to secure near-term power stability while still building a credible low-carbon path for the medium and long term.

My view is that the time cost of extension and restart is simply too high for either to serve as the main solution. Taiwan should instead accelerate renewables, storage, and grid resilience while beginning serious preparation for next-generation nuclear technologies. That is how Taiwan preserves a low-carbon baseload option after 2035. Energy transition is not a slogan. It is a long-distance balancing act across technology, price, and social consensus.

能源政策:再生能源的挑戰與核能的再思考(2025 再版)

中文版本

前言

2021 年,我曾寫過一篇《能源政策:再生能源的困境和核能的妥協》,以國際能源結構為參照,推演台灣能源轉型的可能路徑。四年過去,全球能源局勢、技術成本與政策態度都歷經巨變 ,台灣也面臨新的十字路口:再生能源增速不如預期、天然氣依賴更深、核三延役公投成為政治焦點。

這篇文章,我沿用 2021 年的分析,借助 chatGPT 延續框架並擴寫,整合最新國際數據、台灣現況與政策爭議,重寫成 2025 再版,既是檢視,也為未來提出更具體可行的能源策略。

各國能源配置與現況(2024)

依照慣例,先看一下各國在2024年的能源配置,推薦可以到這個網站自己看看其他國家的能源分佈,整理的很清楚。

美國:

「頁岩氣優勢仍在,天然氣佔比維持四成,風光持續增長,核能穩定在兩成左右」

天然氣約 39%、核能 19%、再生能源 23%、燃煤 18%。

歐盟:

「零碳排為主線,風光占比快速上升,多國重新評估核能定位」

再生能源高達 42%、核能 24%;化石燃料中燃煤與天然氣各佔約 15%、19%。

德國:

「已全面非核,風光合計逾五成,煤炭因能源安全需求短期反彈」

再生能源 52%,煤 27%、天然氣 17%。

法國:

「依然是全球核電比例最高的國家」

核能依然占主導(68%)。再生約 24%,煤 2%、天然氣 6%。

日本:

「重啟多座核電機組,視為減碳與能源安全雙保險」

再生 25%、核能 10%、天然氣 28%、煤 27%。

韓國:

「延長核電機組服役,並推動海上風電」

核能 27%、再生 8%、煤 35%、天然氣 28%。

台灣能源現況(2024 年台電統計)

- 天然氣:約 44%(高於 2020 年的 40.8%)

- 煤炭:約 31%(下降但仍高於三成)

- 核能:約 9%(核二除役、核三剛除役)

- 再生能源:約 9–10%(離岸風電 2–3%、太陽能 5–6%)

- 2024 年:天然氣 44%、煤炭 31%、核能 9%、再生能源 9.5%、其他約 6.5%。

- 2020 年:天然氣 40.8%、煤炭 36.4%、核能 12.7%、再生能源 5.8%、其他約 4.3%。

觀察

- 再生能源比例雖較三年前翻倍,但仍遠低於 2025 年官方 20% 的目標。

- 天然氣進口依賴度高且受國際 LNG 價格波動影響顯著。

- 核三延役討論熱度升高,但依舊缺乏。

能源別分析與 2025 建議立場

火力發電

- 天然氣短期內仍是基載核心(2025–2030 年占比 40–45%),煤炭則應進一步壓至 25% 以下。

- 建議與國際 LNG 長約鎖價,減少進口成本波動影響。

再生能源

- 短期目標:2025–2030 再生能源占比由 9.5% 提升至 20%。

- 電力網與儲能建設必須同步加速,避免再生能源產能因併網不及而浪費。

- 電價政策應合理化,把補助資源導向基礎設施而不只是高額電價補貼。

核能

- 不建議延役核三與重啟核四:延役或重啟的關鍵,不是政治口號,而是耗時與耗費的現實。根據核一先前的送件紀錄,僅核安會的安全審查就長達 7 年。若資料屬實,核三延役將無法及時銜接供電缺口,與重啟核四一樣,存在時程過長、技術門檻高、社會接受度低與安全疑慮未解等問題。

- 策略方向:不應再投入資源在大型傳統核電,應將研發與制度資源轉向小型模組化反應爐(SMR)等新世代核能,為 2035 年後提供穩定低碳備援選項。

Recap My Observation in 2021

核四議題

撇除爭議不小的工程與安全性問題,以下將單就整體能源配置的方向切入,並分析核四重啟是否必要?

再生能源目前約貢獻5–6%,而核四若重啟約能貢獻5%的電量,雖核四可作為基載能源,但台灣目前尚有燃氣與燃煤可作穩定能源,故並不缺乏基載能源。因此核四重啟所需年限與再生能源成長速度便成為關鍵。

目前核四最尷尬的位置在於,重啟時間若無法有效銜接核二核三的除役,便會面臨2025核能清零後,2030年又冒出5%的核四電力,此缺口對於能源規劃將造成諸多困難,除了由於福島核災而勒令停止國內多數核電廠的日本,目前並未看到其餘國家在核能政策的規劃上有髮夾彎的情況發生。(日本目前核能占比6%,計畫2030年重回20%)

觀察各國再生能源的發展便可發現,若搭配政府大力扶持,十年內翻倍成長並不少見,且多數是在2010到2020的十年內由10%左右翻倍至20%。考慮到台灣並不落後的環境條件(風場與日照),與現今較低的再生能源基數,十年內成長至10%佔比並非不可能。若估計核四需要七年重啟並貢獻目前5%的佔比,再生能源在七年內翻倍成長便能補足此差額,若成長過緩可考慮延役核三換取時間。(意即唯一延長核三服役的情況是再生能源發展過緩)

總結

台灣的能源轉型,不能靠單一能源解決所有問題。2025 年的核三延役公投,雖然吸引了輿論與政治焦點,但真正的難題是如何在短期內穩定供電,同時為中長期低碳轉型鋪路。

我的判斷是,延役與重啟的時間成本過高,不應作為主力方案,而應全力加速再生能源、儲能與電網韌性建設,同時啟動新世代核能的研發準備,讓台灣在 2035 年後仍有低碳基載選擇。能源轉型不是口號,而是必須持續在技術、價格與社會共識之間找到平衡的長跑。